What is Founder Vesting?

Founder vesting is a term used to describe an arrangement among startup founders that limits their control over company shares as time progresses. Under this arrangement, founders get their stock assigned upfront but are entitled to these shares incrementally, over a span of typically 2 to 4 years.

The primary purpose of founder vesting is to align incentives and encourage long-term commitment to the company. Without vesting, founders could leave with their full equity stake even if they depart early on. Vesting incentivizes founders to stay for the long haul and earn their full allocation of shares.

Here's how founder vesting typically works:

- Founders receive an upfront grant of stock when the company is formed. For example, a founder may get 1 million shares.

- The founder's shares are initially all unvested. This means the shares are at risk of being forfeited if the founder leaves.

- Over the vesting period (e.g. 4 years), a portion of the shares vest each month or quarter. For example, 1/48th may vest monthly over 4 years.

- Once shares are vested, the founder owns them outright and keeps them if they leave the company. Unvested shares are forfeited if the founder departs.

- A one-year cliff is common, where no shares vest for the first year. Then vesting kicks in on a monthly or quarterly basis.

By gradually earning their equity stake over time, a founder's stock vesting powerfully aligns incentives. Founders are motivated to add long-term value, not just short-term gains. This retention mechanism boosts the resilience and success of startups.

Importance of Founder Vesting

Founder vesting is a crucial component in building a successful startup for several reasons:

Retaining Talent

Vesting ensures that founders earn their equity stake over time through continued contributions. This incentivizes founders to keep working hard to build the company rather than resting on their laurels. Without vesting, founders could leave soon after getting their full equity, depriving the company of their skills and know-how. Vesting aligns incentives by tying the founders shares' rewards to their ongoing participation.

Avoiding Free Riders

Vesting protects against "free riders" - founders who leave early with substantial equity despite minimal contributions. For instance, a founder may put in 6 months of initial work and then depart with their full 10% stake. With the new vesting schedule in place, they would only get a portion of shares tied to their time served. Vesting ensures equity splits reflect actual contributions over the long-term.

Protecting the Company

Vesting gives companies leverage if a founder becomes uncooperative or negligent. Rather than being stuck with a disengaged founder with substantial equity, unvested shares can be repurchased. This minimizes potential damage from founders who lose motivation or no longer add value. Proper vesting terms prevent companies and other shareholders from being held hostage by errant founders.

Determining Founder Equity Splits

When starting a company with multiple founders, one of the most important early decisions is determining how to split equity ownership among the founding team. This split lays the foundation for the company's ownership structure and cap table. While there's no one-size-fits-all formula, there are some best practices founders should consider.

The most common factors to weigh when dividing founder equity include:

- Roles and responsibilities - Founders taking on more essential roles like CEO or CFO often receive larger equity stakes. Typical CEO stakes range from 20-50%, CTOs 15-35%, and other roles 10-30%.

- Contributions - Founders who contribute more in terms of ideas, intellectual property, relationships, capital, or sweat equity may merit higher equity. Vesting schedules can help balance unequal contributions.

- Commitment - Full-time founders tend to get larger stakes than part-time founders. Vesting gives full-timers an upside for their greater commitment.

- Risk - Founders taking on more financial risk or reputational risk deserve greater equity compensation for the additional downside exposure.

- Vision & purpose - Founders providing the core vision, passion, and purpose for the venture often receive larger stakes.

- Negotiating leverage - Founders with specialized skills, access to resources/capital, or alternative options hold more leverage in equity negotiations.

- Future role - A founder's intended future role impacts their equity stake. A smaller % for a future advisor role vs a larger % for an ongoing executive role.

There's no perfect formula, but being thoughtful about equity splits and vesting early on prevents issues down the road. Founders must balance rewarding contributions fairly while retaining talent for the long run.

Standard Vesting Schedules

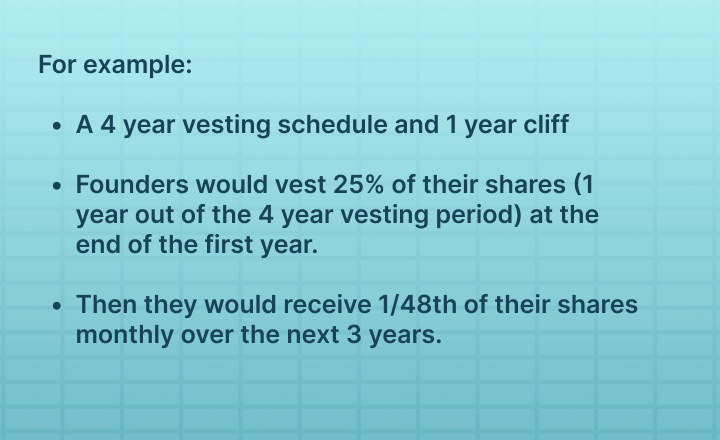

Founders should establish a standard vesting schedule for their equity at the business plan outset. This defines the timeframe over which founders will earn full rights to their shares. Typical vesting schedules last 4 years with a 1-year cliff.

This means founders do not earn any vested shares during the 1 year cliff period. After the first year, they begin vesting their shares on a monthly or quarterly basis over the remaining 3-year period.

The cliff period is important because it incentivizes founders to commit for the long-term. If a founder leaves before the 1-year cliff, they walk away with no vested equity.

Vesting schedules may also include acceleration clauses. These allow founders to add vesting of shares faster upon certain events like an acquisition, being terminated without cause, or hitting growth milestones.

Overall, standard vesting ensures founders earn their equity over time while protecting the company from early departures. The typical reasonable vesting schedule aligns incentives and sets clear expectations.

The Significance of Cliff Periods

A vesting cliff period refers to the initial timeframe in a founder's vesting schedule during which none of their shares vest. Often set at 1 year, the cliff period is an important provision that aligns incentives and deters founders from leaving too quickly.

The rationale behind cliff periods is to ensure founders have "skin in the game" for an initial substantial period as the company gets off the ground. If founders were allowed to take vesting restrictions out right away, they could leave after a short enough time period and still walk away with significant equity.

Cliff periods incentivize founders to stick around for at least the initial critical phase of the startup journey. Knowing their shares won't begin vesting until after 1 year motivates founders to fully dedicate themselves to the venture.

The implications of a founder leaving before the cliff period are drastic - they forfeit all of their unvested shares. While this may seem harsh, it prevents a lack of commitment. Founders who make it through the demanding first year demonstrate their dedication to the startup.

Overall, cliff periods are an important alignment tool. They give comfort to co-founders and investors that the team is committed to the long haul. Founders should understand cliff implications to avoid painful surprises if departing too soon.

Treatment of Unvested Shares Upon Acquisition and Termination

Founder vesting offers an advantage in dealing with shares in specific situations such as an acquisition or the termination of a founder.

Acquisition of the Company

If a startup gets bought out before the founder's shares are completely vested, there are a couple of outcomes for those unvested shares:

- The company acquiring might choose to speed up the vesting process for all shares making them fully vested once the acquisition is finalized. This is commonly done to motivate founders to remain actively involved during the transition.

- The unvested shares are converted into shares of the acquiring company, subject to the founder's original vesting schedule.

- The unvested shares are purchased back by the startup at their fair market value before the acquisition closes. The founder would keep any vested shares.

- The unvested shares are simply canceled or forfeited, providing no payout to the founder for those shares.

The specific treatment is usually outlined in the acquisition agreements and heavily negotiated.

Founder Leaves the Company

If a founder leaves or is let go before they fully own their shares, the company can choose to buy or cancel their shares depending on the reasons for their departure.

This introduces the concepts of "good leaver" vs "bad leaver":

- Good Leaver: If the founder decides to depart on their terms or in a mutual-separation, they are usually considered a "good leaver." In these instances, the company commonly buys back any shares at a fair price. This provides some compensation to the founder.

- Bad Leaver: If the founder is fired for cause or violates their agreement, they can be classified as a "bad leaver." Here, the unvested shares are usually canceled outright without any payout.

Proper founder vesting provisions protect the company from an adversarial founder departure, while still providing fair treatment for cooperative founders who move on amicably. Defining good and bad leavers is key.

Protecting Control via Vesting

Founders have several options to protect control of their company even as their shares vest over time. Three common mechanisms are leveraging supervoting shares, implementing transfer restrictions, and rights of first refusal when allocating stock.

Supervoting Shares

Instead of assigning all the founder's shares to the same common stock class, founders have the option to create a distinct category of supervoting shares with increased voting rights per share. This allows the founders to hold onto the supervoting shares that grant them voting authority and influence. As regular common shares subject to vesting move over the vesting schedule, the founders maintain their heightened voting rights through their supervoting shares. This prevents dilution of control.

Transfer Restrictions

Transfer restrictions limit founders' ability to sell or purchase shares or transfer unvested shares. Often founders cannot sell or transfer any shares, vested or unvested stock, without approval from the board of directors or a shareholder vote. Transfer restrictions ensure founders don't offload large numbers of shares before vesting terms are satisfied.

Rights of First Refusal

Rights of first refusal give common shareholders of the company the option to purchase any shares a founder wants to sell, usually at fair market value. This prevents founders from selling a certain percentage of their equity to outside parties and maintains existing ownership and control dynamics. Rights of first refusal help curb potential issues with founders transferring shares before vesting is completed.

Vesting protects startups, but mechanisms like supervoting shares, transfer restrictions, and rights of first refusal help protect founders' control as well. Founders should consider these options when negotiating vesting terms.

Negotiating Vesting with Investors

Investors in startups, including venture capitalists, typically look for founders to have a vesting plan before they decide to invest. The idea behind this is to make sure that the founders are dedicated to the company for the haul and motivated to drive its growth.

Here are some tips when negotiating vesting with investors:

- Make sure you're ready for a four-year vesting plan with a one-year waiting period before any benefits kick in. Most investors will expect this baseline.

- Try to minimize any additional vesting requirements investors propose. If they want an additional year of vesting for founders, see if you can negotiate down to 6 months.

- Make sure all founders are subject to the same vesting terms. No special treatment for CEOs or other co-founders.

- Seek acceleration provisions that allow some equity to vest early if the company hits key milestones. This aligns with incentives.

- Vesting should accelerate fully upon a sale or IPO. Make sure this is part of the terms.

- Require investor approval for any vesting changes post-investment. Don't let your equity be diluted.

- Seek to exempt a small portion of founders' equity from vesting (10-20%). This provides some protection.

- Get experienced legal counsel to review the proposed terms. Vesting has major implications.

With thoughtful negotiation and compromise, founders and potential investors can agree upon fair vesting terms that work for all parties involved. Being flexible while also clearly communicating your interests is key.

Tax and Legal Considerations of Founder Vesting

Founder vesting has important tax and legal implications that must be considered.

Tax Implications

The tax treatment of founder stock and equity is complex. When stock vests and founders receive shares, it is generally considered taxable income. The value of the shares at the time of vesting determines the amount of income recognized. Founders are then responsible for paying taxes on this income.

There are strategies to reduce the tax load, like opting for 83(b) elections or delaying tax payments. It's essential to seek advice from a tax consultant to enhance tax planning and submissions related to founder vesting.

Securities Laws

Founder vesting arrangements must comply with federal and state securities laws. The offer and sale of stock to founders is considered a securities transaction. Care must be taken to either qualify for an exemption or register the securities appropriately.

Legal counsel that specializes in securities regulations should review any founder vesting terms before they are finalized and executed. This helps avoid noncompliance issues down the road.

Importance of Documentation

Proper documentation is critical when implementing founder vesting. This includes stock purchase agreements, restricted stock agreements, bylaws, shareholder agreements, and 83(b) elections.

Ensuring that the necessary legal documents are in place is crucial to defining founder vesting for both the company and its founders. By planning and documenting everything from the beginning, potential uncertainties and disputes can be avoided.

Founder Vesting Case Studies

When founder vesting is implemented carefully it can align incentives, and keep individuals engaged in a startup. Yet, if not structured correctly it may result in disagreements. Examining real-world examples provides valuable lessons for founders.

Good Founder Vesting Example

Social media startup Snapchat implemented founder vesting successfully. The three co-founders Evan Spiegel, Bobby Murphy, and Reggie Brown agreed to a vesting schedule where their shares vested over 3 years with a 1-year cliff.

When Brown left the company early on, Snapchat exercised its right to repurchase Brown's unvested shares. This protected the interests of the remaining founders Spiegel and Murphy and aligned incentives going forward. Snapchat's thoughtful founder vesting enabled the startup to move forward smoothly after a founder's departure.

Problematic Founder Vesting Scenario

In contrast, communications company Ooma structured founder vesting in a way that later caused disputes. Ooma had two co-founders, Andrew Frame and Peter Prasad. Prasad left Ooma after 2 years, before fully vesting.

Frame argued that Prasad's unvested shares should be voided. However, Ooma's agreements had no provisions for what happens when a founder departs pre-vesting. The lack of clarity led to a lengthy legal battle between the founders.

Key Lessons

These examples highlight the importance of carefully constructing founder vesting terms upfront. Vesting should clearly outline the equity split, vesting schedule, treatment of unvested founder shares thereafter, and contingency plans. Vague founder agreements can lead to conflict later. Proper founder vesting alignment enables smooth sailing even when founders depart.