Introduction to Leveraged Buyouts (LBOs)

A leveraged buyout (LBO) is a transaction in which a company or business is acquired using a significant amount of borrowed money (leverage) to meet the cost of acquisition. In an LBO, a financial sponsor, typically a private equity firm, acquires a controlling interest in a company's equity, while also assuming a substantial amount of debt. This debt is then serviced using the target company's future cash flows, with the ultimate goal of generating high returns on the equity investment.

LBOs have played a pivotal role in the evolution of the modern financial landscape, particularly in the realm of private equity and mergers and acquisitions (M&A). These transactions have enabled private equity firms to acquire and restructure undervalued or underperforming companies, with the aim of improving their operations, finances, and overall value.

The concept of leveraged buyouts can be traced back to the late 1970s and early 1980s, when a wave of hostile takeovers and corporate raids swept across the United States. Pioneering firms like KKR paved the way for the use of debt financing to acquire companies, often against the wishes of incumbent management. This period saw the emergence of the ""corporate raider"" figure, as well as the development of innovative financing techniques, such as the use of high-yield (junk) bonds.

Over the years, LBOs have evolved from their contentious beginnings to become a widely accepted and sophisticated investment strategy. Today, they are employed by a diverse range of financial sponsors, including private equity firms, sovereign wealth funds, and even corporate entities, as a means of acquiring and restructuring businesses for long-term value creation.

How Does a Leveraged Buyout Work?

A leveraged buyout is a complex process involving multiple parties and a series of structured steps. Here's how a typical LBO unfolds:

1.Target Identification

Private equity firms, often working with investment banks, identify a potential target company that meets specific criteria, such as strong cash flow, growth potential, and operational inefficiencies that can be improved.

2. Due Diligence

The private equity firm conducts extensive due diligence on the target company, analyzing its financials, operations, management team, and industry dynamics. This process helps assess the company's value and potential for improvement.

3. Deal Structuring

If the target company is deemed suitable, the private equity firm structures the deal, determining the purchase price, financing sources, and the optimal capital structure for the acquired company.

4. Financing Arrangements

The private equity firm secures financing from various sources, including debt and equity. Debt financing, typically consisting of senior debt, subordinated debt, and mezzanine financing, provides the majority of the capital required for the acquisition.

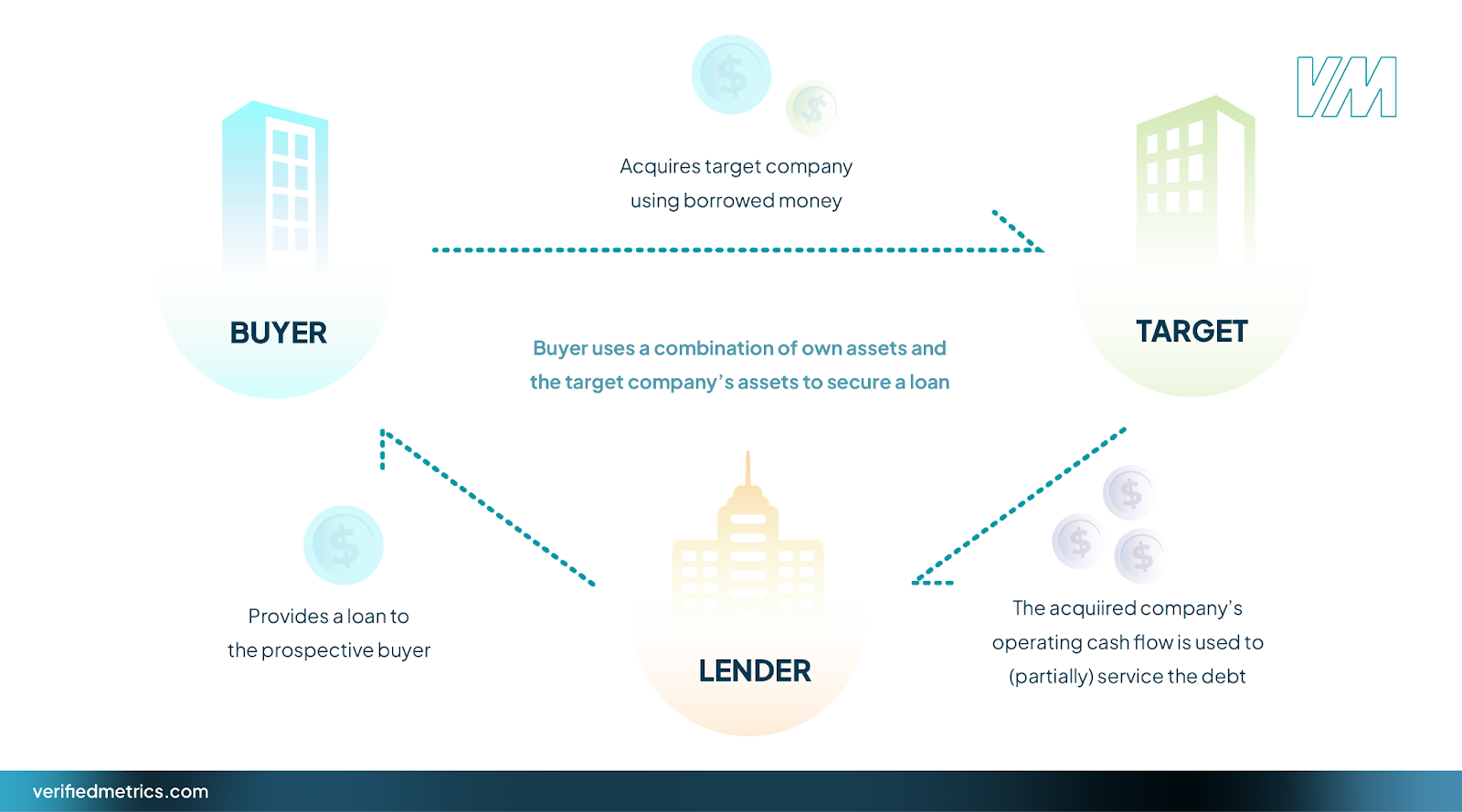

5. Acquisition

The private equity firm, often through a newly formed acquisition vehicle or holding company, acquires the target company using the secured financing and its own equity contribution.

6. Post-Acquisition Restructuring

After the acquisition, the private equity firm implements strategic and operational changes to improve the acquired company's performance. This may involve cost-cutting measures, streamlining operations, divesting non-core assets, and implementing new management practices.

7. Debt Repayment

The acquired company's cash flow is used to service and repay the debt incurred during the LBO. This process, known as de-leveraging, aims to reduce the company's debt burden over time.

8. Value Creation

Through operational improvements, strategic realignments, and financial restructuring, the private equity firm works to increase the acquired company's value and profitability.

9. Exit Strategy

After a predetermined holding period, typically 3-7 years, the private equity firm explores exit strategies, such as an initial public offering (IPO) or a sale to another company or investor. The goal is to maximize returns on the investment.

Key players involved in an LBO include:

Private Equity Firms

These firms initiate and lead the LBO process, providing the equity capital and expertise to acquire and restructure the target company.

Target Company

The company being acquired through the LBO process.

Investment Banks

These banks assist with deal structuring, financing arrangements, and advisory services.

Lenders

Various lenders, such as banks, institutional investors, and specialized debt providers, provide the debt financing required for the LBO.

Management Team

The existing or new management team plays a crucial role in implementing the operational and strategic changes post-acquisition.

Advisors

The accountants, lawyers and consultants that help to diligence and structure the transaction

The LBO process is complex and involves significant financial engineering, risk management, and strategic planning to maximize returns for the private equity firm and create value for the acquired company.

Financing an LBO

Leveraged buyouts gain their name because they rely heavily on debt financing to fund the acquisition of the target company. In a typical LBO, the acquiring firm or private equity fund will contribute a relatively small portion of equity, usually ranging from 10% to 30% of the total purchase price. The remaining 70% to 90% of the required capital is raised through various forms of debt financing.

Debt financing plays a critical role in LBOs because it allows the acquirer to gain control of a much larger asset base with a relatively small equity investment. This leverage amplifies the potential returns on the equity invested, but it also increases the risk associated with the transaction.

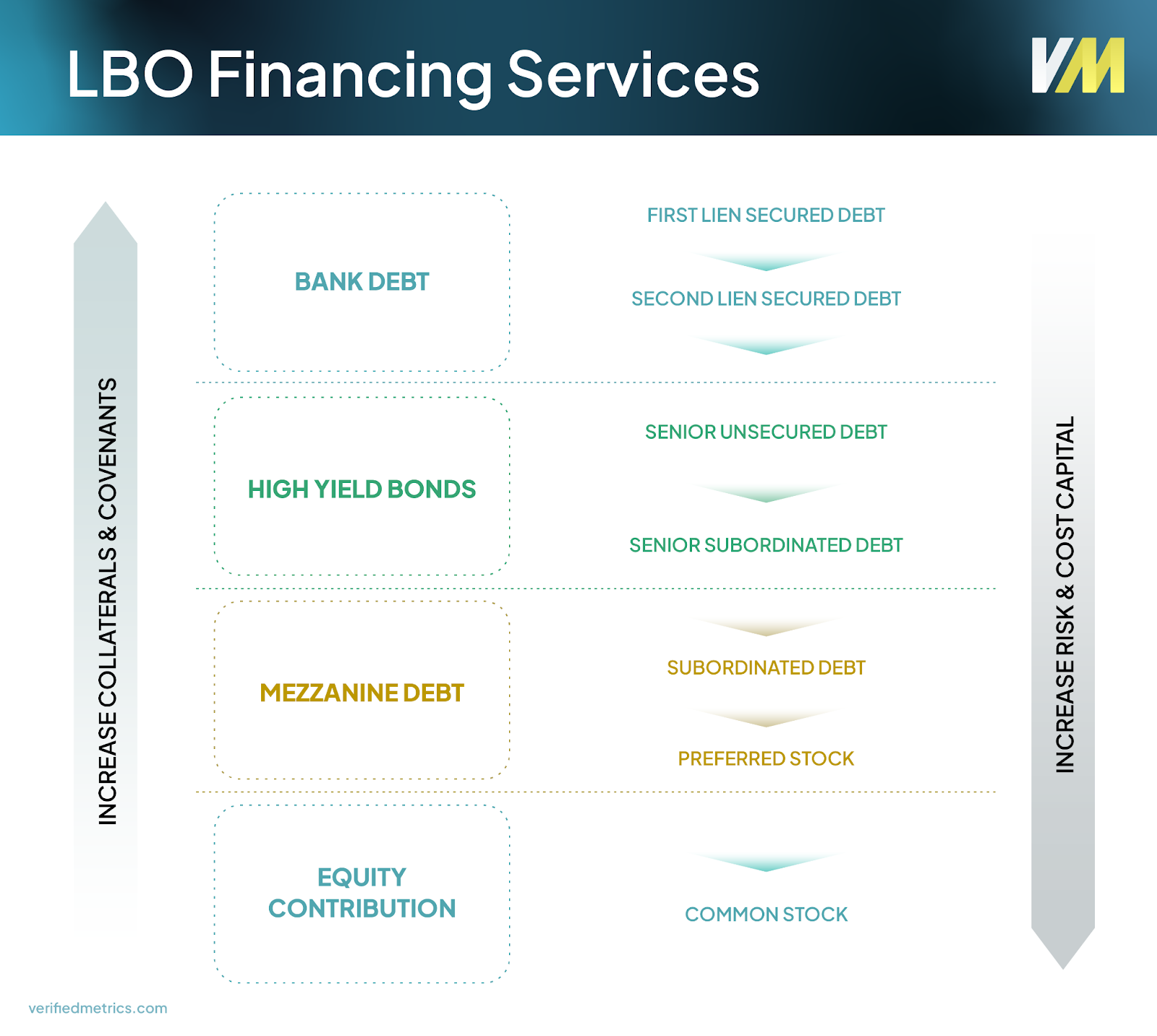

Several types of debt are commonly used to finance LBOs, each with its own characteristics and risk profile:

1. Senior Debt

Senior debt, typically provided by banks or other financial institutions, is the primary source of debt financing in LBOs. This type of debt has the highest priority in terms of repayment and is secured by the assets of the target company. Senior debt typically accounts for a significant portion of the total debt financing in an LBO.

2. Subordinated Debt

Also known as junior debt or mezzanine financing, subordinated debt has a lower priority for repayment than senior debt. It is often used to bridge the gap between the amount of senior debt available and the total financing required. Subordinated debt typically carries higher interest rates than senior debt to compensate for the increased risk.

3. High-Yield Bonds

In larger LBO transactions, the acquirer may issue high-yield bonds, also known as junk bonds, to raise additional debt financing. These bonds offer higher interest rates to investors to compensate for the higher risk associated with the leveraged capital structure of the acquired company.

While debt financing provides the majority of the capital required for an LBO, the equity contribution from the acquiring firm or private equity fund is also crucial. This equity investment, typically ranging from 10% to 30% of the purchase price, serves several important purposes:

1. Alignment of Interests

The equity contribution ensures that the acquirer has a significant financial stake in the success of the acquired company, aligning their interests with those of other stakeholders, such as lenders and management.

2. Downside Protection

The equity contribution acts as a buffer against potential losses, providing a cushion for the debt holders in the event of underperformance or financial distress.

3. Operational Expertise

Private equity firms often contribute not only capital but also operational expertise and management resources to help improve the performance of the acquired company, enhancing the chances of a successful exit and maximizing returns.

By carefully structuring the debt and equity components of an LBO, acquirers can leverage their capital to gain control of larger assets while managing risk and aligning incentives for long-term success.

Why Do LBOs Occur?

Leveraged buyouts are pursued for a variety of strategic reasons by both private equity firms and the target companies themselves. During periods of low interest rates, LBOs give investors a chance to arbitrage between the cost of financing and the free cash flow generated by the acquired company.

By acquiring a company using a significant amount of debt financing, private equity firms can minimize the amount of equity they need to contribute. This leverage amplifies their potential returns if the acquired company performs well and increases in value. Additionally, private equity firms often seek out undervalued or underperforming companies as LBO targets, with the intention of implementing operational improvements and strategic changes to unlock hidden value.

For target companies, being acquired through an LBO can provide several benefits. First, it offers a way for the company's existing owners or shareholders to cash out their investments, either partially or entirely. This can be particularly appealing for founders, family-owned businesses, or companies looking to transition ownership.

Moreover, LBOs can provide target companies with access to additional capital and resources that may not have been available as a standalone entity. Private equity firms often have extensive industry expertise and management experience, which can be leveraged to drive operational efficiencies, streamline processes, and implement strategic initiatives.

LBOs can also serve as a catalyst for significant organizational changes within the target company. Private equity firms may restructure the company's operations, divest non-core assets, or pursue strategic acquisitions or mergers to enhance the company's competitive position and growth prospects.

Overall, LBOs occur because they offer potential benefits to both private equity firms seeking attractive investment opportunities and target companies looking for strategic partners, access to capital, or a pathway to transition ownership.

Characteristics of Companies Suitable for LBOs

Successful leveraged buyouts typically target companies with specific financial and operational characteristics that make them attractive acquisition targets. These traits not only increase the likelihood of securing debt financing but also provide opportunities for value creation after the buyout.

From a financial perspective, ideal LBO targets are companies with strong and stable cash flows. Robust cash flow generation is crucial for servicing the significant debt burden that comes with an LBO. Companies with predictable revenue streams, high profit margins, and low capital expenditure requirements are particularly appealing.

Additionally, companies with low debt levels and substantial tangible assets are favored LBO targets. Tangible assets, such as real estate, equipment, or intellectual property, can be used as collateral to secure debt financing. Low existing debt also means less competition for cash flows when repaying the acquisition-related debt.

Operationally, companies with opportunities for improvement are often sought after for LBOs. Private equity firms aim to identify companies with potential for cost-cutting, operational streamlining, or strategic realignment. Companies with inefficient processes, underutilized assets, or untapped growth opportunities can benefit from the operational expertise and financial resources provided by the private equity acquirer.

Examples of successful LBO targets that exhibit these characteristics include mature, market-leading companies in industries such as consumer goods, healthcare, and business services. For instance, the iconic LBO of Hilton Hotels by Blackstone Group in 2007 targeted a company with strong cash flows, valuable real estate assets, and opportunities for operational improvements.

Another notable example is the LBO of Dunkin' Brands by private equity firms Bain Capital, Carlyle Group, and Thomas H. Lee Partners in 2005. Dunkin' Donuts and Baskin-Robbins, the two brands under Dunkin' Brands, had steady cash flows, recognizable brands, and potential for expansion and cost optimization.

By targeting companies with these favorable financial and operational characteristics, private equity firms increase the chances of securing debt financing, implementing value-creation strategies, and ultimately generating attractive returns for their investors through an LBO.

Advantages and Criticisms of LBOs

Leveraged buyouts can offer significant advantages, but they also carry inherent risks and criticisms. On the positive side, LBOs have the potential to generate substantial returns for private equity firms and investors. By utilizing debt financing and implementing operational improvements, LBOs can unlock value and drive profitability in the acquired company. Additionally, the high levels of debt involved in an LBO create a sense of urgency and discipline, motivating management to focus on efficiency and cash flow generation.

However, LBOs are not without their drawbacks and criticisms. The high debt burden assumed during an LBO can put significant financial strain on the acquired company, increasing the risk of default or bankruptcy if the business underperforms or faces unexpected challenges. Critics argue that the intense pressure to service debt and generate returns can lead to cost-cutting measures that compromise long-term sustainability, such as layoffs, reduced investment in research and development, and neglect of customer service.

Furthermore, LBOs have faced criticism for their potential impact on employees, communities, and broader stakeholders. Job losses and restructuring efforts are common in LBOs, as private equity firms seek to streamline operations and reduce costs. This can have adverse effects on local economies and disrupt the lives of workers and their families.

Despite these criticisms, proponents of LBOs argue that the potential rewards outweigh the risks, particularly when executed by experienced private equity firms with a proven track record of successful turnarounds and value creation. Ultimately, the success or failure of an LBO depends on various factors, including the quality of due diligence, the strength of the target company's business model, and the ability of the new owners to effectively manage and optimize operations.

How LBOs Create Value

Leveraged buyouts are designed to create value for the private equity firms and investors involved. There are three main ways in which LBOs generate value: operational improvements, strategic realignments, and financial restructuring.

Operational Improvements

One of the primary value creation strategies in LBOs is to drive operational improvements in the acquired company. Private equity firms often bring in experienced management teams and advisors to identify areas for cost-cutting, increased efficiency, and productivity enhancements. These operational improvements can include:

- Streamlining processes and eliminating redundancies

- Optimizing supply chains and procurement practices

- Rationalizing product lines and focusing on core competencies

- Implementing lean manufacturing or service delivery models

- Improving sales and marketing strategies

- Reducing overhead costs and unnecessary expenses

By making the acquired company leaner and more efficient, private equity firms can boost profitability and cash flow, which ultimately increases the company's value.

Strategic Realignments

LBOs also create value through strategic realignments of the acquired company's business model or portfolio. Private equity firms pursue strategies such as:

- Divesting non-core or underperforming business units

- Acquiring complementary businesses to achieve synergies

- Expanding into new markets or product lines

- Refocusing the company on its core strengths and competencies

- Implementing new growth strategies or business models

These strategic realignments can unlock value by concentrating resources on the most promising areas, eliminating distractions, and positioning the company for long-term growth and profitability.

Financial Restructuring

The third way LBOs create value is through financial restructuring. Private equity firms often use leverage (debt financing) to acquire companies, which can provide significant tax benefits and increase returns on equity. Financial restructuring strategies may include:

- Optimizing the capital structure by adjusting debt and equity levels

- Refinancing existing debt at more favorable terms

- Implementing tax-efficient structures and strategies

- Realizing tax benefits from interest expense deductions

- Distributing excess cash flow to equity holders

By skillfully managing the company's financial structure and leveraging tax advantages, private equity firms can enhance the returns on their investment and create value for themselves and their investors.

Ultimately, the combination of operational improvements, strategic realignments, and financial restructuring can significantly increase the acquired company's profitability, cash flow, and overall value. This value creation is the driving force behind leveraged buyouts and the reason why private equity firms pursue these transactions.

LBO Exit Strategies

Executing a successful exit strategy is crucial in a leveraged buyout (LBO) to maximize returns for the private equity firm and its investors. Common exit routes include an initial public offering (IPO), a sale to another company (trade sale), or a secondary buyout by another private equity firm.

Initial Public Offering (IPO)

An IPO is a popular exit strategy that involves taking the acquired company public by listing its shares on a stock exchange. This route allows the private equity firm to cash out its investment by selling its shares to public investors. IPOs are typically pursued when market conditions are favorable and the company has achieved significant growth and profitability.

Trade Sale

A trade sale involves selling the acquired company to a strategic buyer, often a larger corporation operating in the same industry or a related sector. This exit route is attractive when the buyer can realize synergies by integrating the acquired company into its operations, leading to cost savings or revenue enhancements.

Secondary Buyout

In a secondary buyout, another private equity firm purchases the acquired company from the original private equity firm. This exit strategy is common when the original firm believes it has maximized the value creation potential and another firm sees an opportunity for further improvements or growth.

Timing and Execution

The timing of an exit is crucial and depends on various factors, including market conditions, the company's performance, and the investment horizon of the private equity firm. Typically, private equity firms aim to exit their investments within 3 to 7 years, allowing sufficient time for value creation and growth.

Executing a successful exit requires careful planning and preparation. This may involve grooming the acquired company for an IPO by strengthening its management team, improving financial reporting, and ensuring compliance with regulatory requirements. In the case of a trade sale or secondary buyout, the private equity firm will need to identify potential buyers, conduct due diligence, and negotiate favorable terms.

Effective execution of the exit strategy is critical to maximizing returns for the private equity firm and its investors, as it represents the culmination of the value creation efforts undertaken during the LBO process.

Case Study: Dell's Leveraged Buyout in 2013

In 2013, Dell, the renowned computer technology company founded by Michael Dell, underwent one of the largest leveraged buyouts in history. The $24.9 billion deal, led by Michael Dell himself in partnership with private equity firm Silver Lake Partners, marked a significant milestone in the company's journey.

Dell had been a publicly traded company since its initial public offering in 1988. However, by the early 2010s, the company faced mounting challenges in the rapidly evolving technology landscape. The rise of mobile devices and cloud computing had disrupted the traditional personal computer market, which was Dell's core business. To adapt and transform the company, Michael Dell recognized the need for a strategic shift and greater operational flexibility, which a private ownership structure could provide.

The LBO process involved several key players and complex financial arrangements. Michael Dell and Silver Lake Partners formed a consortium to acquire Dell, contributing a combined $4.9 billion in equity. The remaining $19.4 billion was raised through debt financing from various lenders, including Microsoft, which provided a $2 billion loan to support the deal.

The debt financing structure was intricate, involving multiple tranches of loans with varying interest rates and maturities. This included a $13.8 billion senior secured term loan, a $3.25 billion senior secured revolving credit facility, and various other debt instruments. The substantial debt burden placed significant pressure on Dell to generate sufficient cash flow to service and repay the loans over time.

One of the primary objectives of the LBO was to transform Dell from a hardware-focused company into a diversified technology solutions provider. By going private, Dell could more easily restructure its operations, divest non-core businesses, and invest in emerging technologies without the scrutiny and pressures of public markets.

The LBO transaction faced criticism from some shareholders who believed the buyout price undervalued the company. However, Michael Dell and Silver Lake Partners were confident in their ability to unlock value through operational improvements, cost-cutting measures, and strategic refocusing.

In the years following the LBO, Dell underwent significant changes. It streamlined its product portfolio, invested in cloud computing and cybersecurity solutions, and acquired companies like EMC Corporation to expand its enterprise offerings. While the debt burden initially weighed heavily on the company, Dell's strategic initiatives and improved profitability gradually eased the financial strain.

The Dell LBO serves as a notable example of how leveraged buyouts can be used as a tool for corporate transformation and strategic repositioning. By taking the company private, Michael Dell and his partners gained the flexibility to reshape the business model without the pressures of quarterly earnings reports and shareholder demands. However, the success of the LBO hinged on their ability to execute operational improvements, generate sufficient cash flow, and ultimately position Dell for long-term growth and profitability in the evolving technology landscape.

Due Diligence in LBOs

Thorough due diligence is a critical component of any successful leveraged buyout. Due diligence involves an in-depth examination of the target company's financial records, operations, legal compliance, and overall health. This process is essential for identifying potential risks, uncovering hidden liabilities, and ensuring that the acquisition aligns with the buyer's investment strategy.

Traditionally, due diligence in LBOs has been a time-consuming and labor-intensive process, often involving teams of analysts and consultants poring over vast amounts of data and documentation. However, advancements in technology have paved the way for more efficient and streamlined due diligence processes.

Specialist financial due diligence providers like Verified Metrics support deal teams at this stage - preparing quality of earnings analyses, validating the target's financial position, and surfacing the operational issues that drive valuation and negotiation.

Conclusion

Leveraged buyouts (LBOs) have played a significant role in the financial world, reshaping industries and creating opportunities for substantial returns. Throughout this article, we've explored the intricate details of LBOs, from their definition and historical context to the complex processes involved in executing them successfully.

LBOs are powerful financial tools that allow private equity firms and investors to acquire companies using a combination of debt and equity financing. By leveraging debt, these firms can maximize their returns while minimizing their initial capital outlay. However, success ultimately depends on disciplined execution and effective operational and financial management of the acquired company.

One of the key advantages of LBOs is their ability to create value through operational improvements and strategic realignments; private equity firms can unlock the true potential of the acquired companies, driving growth and profitability.

While LBOs have faced criticism for their perceived risks and potential negative impact on employees and stakeholders, it's essential to recognize their role in fostering innovation, promoting competition, and driving economic growth. Successful LBOs have revitalized struggling companies, and created new opportunities for growth and expansion.

As we navigate the ever-evolving financial landscape, understanding the intricacies of LBOs remains crucial for investors, financial professionals, and business leaders alike. By mastering the nuances of these complex transactions, we can better evaluate potential opportunities, mitigate risks, and make informed decisions that drive long-term value creation.

Support for Your Next LBO

Leveraged buyouts are complex transactions that require extensive due diligence to mitigate risks and maximize value creation potential. Verified Metrics provides financial due diligence, valuation, and dataroom services that help deal teams assess targets thoroughly and move through an LBO with confidence.