It’s impossible to exaggerate the importance of market analysis. With the complex connection exhibited by the financial markets, as an investor, you must be intentional about anticipating dangers and assessing stock performances using various financial tools, ratios, and charts.

Investors now examine stock prices and performance using statistical and mathematical ideas. This is where covariance and variance come in handy. These two variables can help you assess volatility, determine the movement of price and any associated risks, etc., on both short-term and long-term basis.

However, the big question now is, how are these two calculations different? This article comprehensively explores covariance vs. variance comparison, including what exactly they are, their benefits, how to calculate them, their differences, and their practical use cases.

Without further ado, let’s dive right in!

First, what is covariance?

Covariance statistically measures how two random variables change in comparison to each other. If high, it shows both variables share a strong relationship; a low covariance means the complete opposite.

In a financial context, it refers to the returns on two investments over a period compared to different variables – stocks, bonds, and other marketable securities.

As an investor, covariance can help you create a balanced risk portfolio. This way, whenever a stock in your portfolio is underperforming, you can be sure there’s another marketable security overperforming, ultimately helping you minimize your financial loss.

There are two types of covariance: positive covariance and negative covariance.

- Positive covariance: If the covariance is positive, the variables under examination tend to go high or low simultaneously. A positive covariance typically slopes upwards. For instance, if variable x and y have a positive covariance, it means whenever x gets higher than average, y does the same, too, and vice versa.

- Negative covariance: We can safely say positive covariance illustrates a direct relationship between two random variables (marketable securities). However, these variables are inversely proportional whenever it is negative – they share an inverse relationship. That is, whenever variable x is more than average, variable x will be less than average, and vice versa. Most investors prefer a negative covariance.

Here is the formula you can use to calculate covariance for variables X and Variables Y:

Cov(X, Y) = Σ(Xi-µ)(Yj-v) / n

Where:

- Cov(X, Y) = the covariance of the examined variables.

- Σ = summation.

- Xi = all values of the Variables X.

- µ = average value of the Variables X.

- Yj = all values of the Variables Y.

- v = average value of the Variables Y.

- n = number of data points collected across Variables X and Variables y.

Benefits of covariance

Undoubtedly, covariance has multiple use cases. But for this article, here are a few investing or business-related benefits associated with the statistical calculation:

- As mentioned earlier, covariance can help you diversify your portfolio. This way, you can develop a reliable risk management strategy while maximizing your possible returns.

- You can use covariance to compare volatility.

- Covariance helps you to analyze the previous price movement of two marketable securities and use that data to predict more accurate future market reactions.

- You can use covariance to determine or identify how a particular security contributes to your portfolio.

What is variance?

In statistics, variance refers to how much a data set deviates from its expected value. In other words, it refers to the width of a distribution. When the distance between the means and the set numbers is large, you’ll have a larger variance, and vice versa.

In a financial context, variance measures the volatility of a company/stock to determine how risky a potential investment may be. Stocks with larger variances are typically riskier than those with smaller variances. However, of course, the higher the risks, the better the returns if it turns out favorable.

Such a security has a fixed value if a variance is neither high nor low but zero. It’s impossible to have a negative value for variance.

Variance is a measure of deviation. It tells you how much security may fluctuate, helping you make better-informed investment decisions.

Here is the formula you can use to calculate variance for variables X and Variables Y:

s2= ∑(x - x̄)/2n - 1

Where:

- s2 = the variance.

- Σ = summation.

- x = each asset returns.

- x̄ = mean.

- n = number of data points.

Benefits of variance

Like covariance, the benefits of variance are also many. However, unlike covariance, variance treats all deviations as the same without considering direction. Here are a few investing or business-related benefits of variance:

- You can monitor your portfolio’s performance using a variance. It helps you identify what is performing badly and how much.

- Variance helps you control cost.

- Variance analysis aids top-management decision-making processes, especially when looking for ways to increase revenue inflow.

- You can also use variance to determine assets' risk and potential profitability.

- Variance’s square root, Standard Deviation, can help you measure an investment’s returns over a given duration.

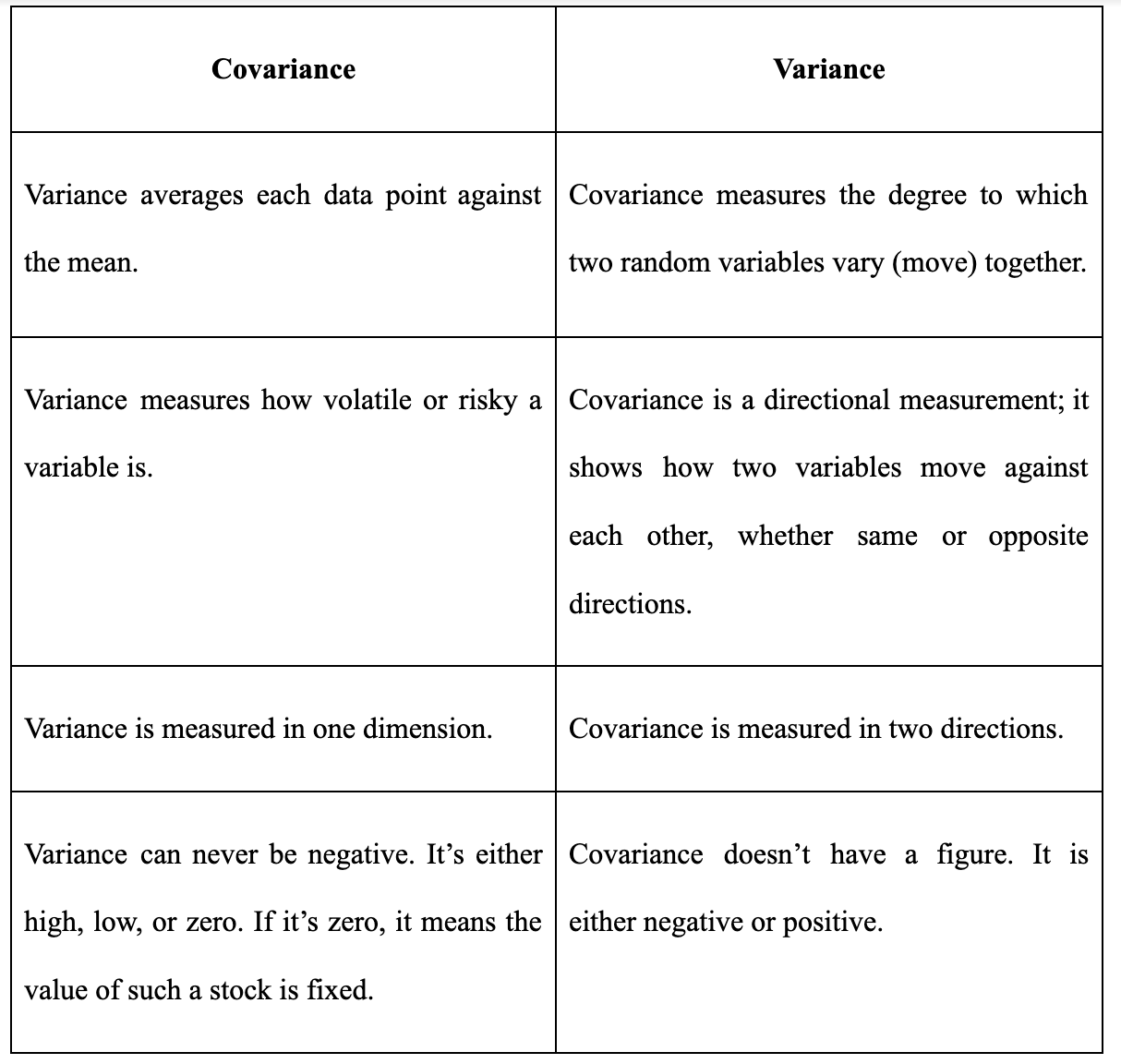

Covariance vs. variance: What are the differences?

Covariance and variance measure the distribution of data points across a calculated mean. But, of course, there are a few differences between variance and covariance. Summarily, while variance measures how the data spread along a single axis, covariance shows the directional relationship between two random variables, X and Y.

For better precision, this article examines these major differences via multiple subheadings:

Meaning

As described earlier in this guide, variance measures deviation – how far each data point moves away from the average (mean). It shows volatility and how risky a particular investment may be. On the contrary, covariance refers to the relationship between two random variables. It describes the direction, whether they move and how far apart such movement is.

Financial context

In the financial world, as an investor or stock portfolio manager, you can use variance to measure how volatile or risky an investment is. This way, you can predict to a considerable extent what may happen to your money due to any investment decision(s) you make.

Contrarily, you can use covariance to measure how the stocks (or other measurable securities) in your portfolio move together or in opposite directions. This way, you can create the right risk management strategy that helps ensure that you have a balanced portfolio.

Variable

Variance measures the variability of each data point in a data set. In other words, the variance of a data set (portfolio) shows how a particular number (stock) varies against the average (mean) value.

For covariance, it shows how two unrelated variables correlate. Covariance measures the “co-variability” of two unrelated stocks, X and Y, in a portfolio.

Indicator

Covariance is not a number. It is either negative or positive. As mentioned earlier in this article, a negative covariance indicates that the two unrelated variables, X and Y, under examination are moving in opposite directions. In contrast, a positive covariance means they move in unison in the same direction.

Unlike covariance, a variance is a number. It measures the magnitude of a random variable (stock). If the variance is low, it means the risk of such a stock – or any other measurable security – is low, and vice versa.

Dimension

Variance focuses on how efficient or inefficient a particular data is. Consequently, it is measured in one dimension. However, since covariance is a directional measurement, it is measured in two dimensions.

Head-to-head table comparison between covariance vs. variance

Examples of covariance in practice

The major use case of covariance is in the finance industry. It helps you to evaluate how much risk is associated with stocks or investments, comparing their direction of movement, whether they move together or against each other.

Many investors also use covariance and correlation side-by-side. It helps determine if and how two marketable securities move together to know whether to add them to their portfolios. You also get to know the factors influencing such movements.

Here is an example of covariance in practice:

Imagine Jay is an investor with a portfolio that primarily tracks S&P 500 performance but wants to add ABC Corp stock to the portfolio. Before adding, he should assess the “directional relationship” (covariance) between S&P 500 and ABC Corp.

If Jay doesn’t evaluate the covariance, he might unknowingly be increasing his portfolio risk. Below is a step-by-step guide to calculating the covariance between S&P 500 and ABC Corp:

- Step 1: Gather data for S&P 500 and ABC Corp. You can’t do anything without the appropriate data.

- Step 2: Calculate each asset’s average (mean) prices.

- Step 3: Calculate the differences between each data point and each asset's average (mean) price.

- Step 4: Using the covariance formula provided earlier in this article, Jay can find the covariance between the two assets.

Examples of variance in practice

Like covariance, variance is also very instrumental in the finance industry. Jay can use the variance equation to determine the individual performance of stocks in his investment portfolio. In other words, variance helps Jay measure how S&P 500, ABC Corp, and other measurable securities in his portfolio perform.

Jay can also use variance to measure risk levels, identifying whether a stock may be worth the purchase. It’s a way to determine uncertainty. Of course, it’s impossible to measure uncertainty expressly, but with variance (and standard deviation), you can get an estimate to inform your investment decision(s).

Here is an example of covariance in practice:

Imagine Jay’s returns for S&P 500 is 10%, 20%, and -15% after the first, second, and third year respectively. These three years give an average of 5% returns – the mean (average value). Consequently, the difference between each return and the average (mean) is 5% in Year 1, 15% in Year 2, and -20% in Year 3.

Square these differences and add them together. Divide 6.5 by 2 (one less the number of years under examination, i.e., 3-1 = 2) to get the variance. Therefore, the variance of the S&P 500 for Year 1, Year 2, and Year 3 is 3.25%. Jay will have a cumulative value of 6.5%.

Below is a step-by-step guide to how Jay has just calculated the variance for the stock S&P 500 for the last three years:

- Step 1: Identify the asset's returns over a specific period of years.

- Step 2: Calculate the mean of the measured returns.

- Step 3: Calculate the difference between each asset’s return and the mean value

- Step 4: Square the differences per year and add the results together.

- Step 5: Divide the result by the total number of data points minus 1. Using the example above, Jay will divide 6.5% by 2.

- Step 6: You can also calculate the standard deviation, the square root of the variance.

If Jay gets a high variance, the risk is high, and vice versa. If it is zero, it means the asset has a fixed value.

Final thoughts on covariance vs. variance comparison

Undoubtedly, both covariance and variance are statistical terms that prove instrumental in the financial and investment world. Although they sound similar, they are quite different. Now, you'll be able to distinguish the two.