Introduction to Full Ratchet Anti-Dilution

A full ratchet anti-dilution provision is a protective clause for investors in startup funding rounds. It is designed to maintain an investor's ownership percentage if a company issues shares at a lower valuation in a future round.

With a full ratchet, if a down round occurs, the conversion price of existing preferred shares is reduced to match the lower price of the new round. This issuance of more shares to the original investor prevents dilution of their stake. The purpose of a full ratchet is to fully protect early investors from dilution in down rounds. It provides strong anti-dilution protection by issuing more shares to these investors if the share price decreases.

Full ratchets benefit investors by allowing them to maintain their proportional ownership in a company, even if valuations fall in later rounds. However, they can impose significant dilution on founders and existing common shareholders.

How Full Ratchet Anti-Dilution Works

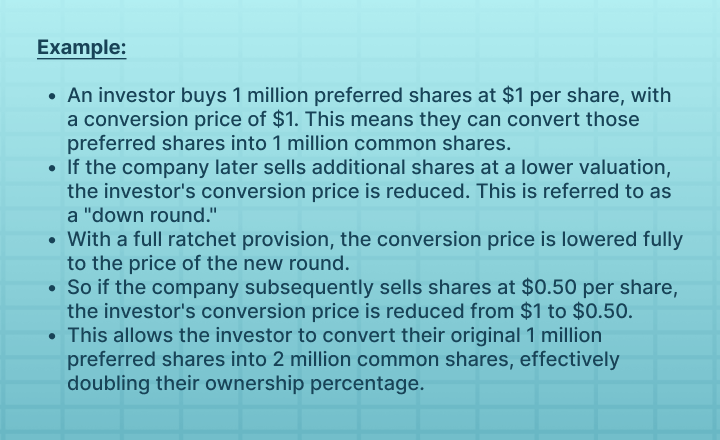

A full ratchet anti-dilution provision is designed to protect investors against dilution of their ownership stake in a company. Here's how it works: When an investor buys preferred shares in a startup, those shares can typically be converted into common shares at a set price, known as the "conversion price."

The full ratchet provision prevents dilution by allowing them to maintain their original proportional stake. Without this full downward ratchet adjustment, the investor would experience dilution since their 1 million shares would become a smaller portion of the total shares outstanding after the new lower-priced round. The full ratchet provision protects against this by adjusting the conversion ratio downward.

Benefits for Investors

Full ratchet anti-dilution provisions offer several key benefits for investors in startup companies. The primary advantage is stronger protection from dilution in future financing rounds. With a full ratchet, investors are able to maintain their proportional ownership stake if the company raises capital at a lower valuation.

For example, if an investor owns 10% of the company after investing at a $10 million valuation, and the next round is at a $5 million valuation, the full ratchet provision will allow the investor to receive enough additional shares to keep their stake at 10%. This prevents the dilution they would otherwise experience. Full ratchets also provide motivation for investors to participate in down rounds. Even though the valuation is lower, investors know their ownership percentage will remain constant. They are more inclined to provide needed capital in challenging times for the startup.

Overall, full ratchets give investors confidence that their stake in the company will not be diluted excessively in the future. By agreeing to a full ratchet, the company enables investors to maintain influence even as valuations fluctuate. This protection encourages investment, especially in high-risk, early-stage ventures.

Risks and Downsides for Companies

It is important to consider all of the factors regarding a full ratchet anti-dilution provision. Before you accept it, here are the following factors to consider:

Loss of Control and Ownership for Founders

One of the biggest risks of agreeing to a full ratchet is potentially the dramatic loss of control and ownership by founders and early employees. Because a full ratchet resets the conversion price fully down to the new lower valuation, founders can see their ownership stakes massively diluted in future rounds. This can enable later-stage investors to gain controlling stakes in the company. Founders can be left with minimal control and financial upside in the businesses they create.

"Death Spiral" Capitalization Scenarios

In extreme cases, an overly broad full ratchet coupled with successive down rounds can create a "death spiral" scenario for a startup. Here, continuing dilution essentially transfers most or all ownership to new investors, making it increasingly unattractive for existing shareholders to participate in future rounds. This can threaten the viability of the company if new capital is cut off. While rare, this risk is why companies should closely evaluate whether full ratchet provisions are absolutely necessary for funding.

Lack of Upside Participation

Weighted average anti-dilution provisions are often viewed as more founder-friendly alternatives to full ratchets. With weighted average, the conversion price is adjusted partially rather than fully down to the new round valuation. This allows founders to maintain more upside potential if the company ultimately succeeds. Full ratchets remove much of this potential upside in the event of growth.

Alternatives to Explore

Rather than accepting broad full ratchet terms, companies can try to negotiate for narrower provisions or different models entirely.

For example, a pay-to-play provision keeps anti-dilution protection only for investors who continue participating in future rounds. Redemption rights allow new investors to be made whole based on a company's performance. Or, companies can argue for omitting full ratchet provisions in early rounds when risk is higher.

Full Ratchet vs. Weighted Average

The two main types of anti-dilution provisions are full ratchet and weighted average. Both protect investors against dilution, but they work differently:

- Full ratchet - If a down round occurs, the conversion price is reduced to the price of the new shares issued. This results in the investor getting more shares to maintain their ownership percentage.

- Weighted average - The conversion price is reduced based on a weighted average of the old conversion price and the new share issuance price. The investor gets additional shares, but less than under a full ratchet.

A full ratchet offers more protection for investors, as their stake is fully protected against any dilution. However, this can significantly dilute existing shareholders. A weighted average causes less dilution of existing shareholders. But investors bear more of the impact of a down round. In high-risk startups, investors may insist on a full ratchet to protect their investment. More mature companies can negotiate a weighted average clause. Some agreements use a hybrid approach:

- Full ratchet if the valuation decreases by more than 20-30%

- Otherwise, use a weighted average

This balances investor protection with minimizing excessive dilution of existing shareholders. The choice depends on negotiations between investors and shareholders. Companies should educate themselves on the implications before agreeing to anti-dilution terms.

Negotiating Full Ratchet Provisions

With adequate preparation and understanding, you can ensure that your negotiation process is successful with both parties understanding the differing perspectives.

Strategies for Founders

For startup founders and company owners, the risks of dilution and loss of control associated with a full ratchet can be concerning. Here are some strategies founders can employ when negotiating full ratchet terms:

- Request a valuation floor or cap on dilution. This sets a limit on how much the conversion price can ratchet down, providing some protection.

- Negotiate a sunset provision or time limit. This would restrict the full ratchet to early investment rounds, reverting to a weighted average ratchet in later rounds.

- Seek exceptions for certain financing events like an IPO or secondary offering that require a lower valuation. This prevents unfair dilution in certain cases.

- Limit the types of events that trigger the ratchet, excluding scenarios like non-cash/non-equity considerations.

- Negotiate the right to redeem shares or remove the full ratchet via a shareholder vote after a certain period. This provides an "out" if needed.

- Require investor consent for the ratchet to be triggered, rather than making it automatic. This gives the founder more control.

Key Points for Investors

Investors will push for a broad full ratchet provision to protect their ownership stake. Some key points they may focus on include:

- Maintaining automatic operation of the ratchet for all future rounds, without needing consent.

- Avoiding valuation floors, which limit the downside protection of the full ratchet.

- Having the ratchet apply to all financing events, not just equity rounds. This includes debt, convertibles, etc.

- Rejecting time limits or sunset provisions on the full ratchet. They will want long-term protection.

- Resisting share redemption rights or removal of the ratchet via shareholder votes.

- Seeking broad language that captures all possible financing events that could trigger dilution.

With reasonable compromises on both sides, founders and investors can strike the right balance of incentives and protections. Being aware of each perspective leads to better negotiations.

Legal and Regulatory Considerations of Full Ratchet Provisions

Full ratchet provisions have important legal and regulatory implications that companies and investors should be aware of when negotiating and implementing these clauses. Here are some key considerations:

Relevant Regulations

- There are many regulations that companies need to ensure that they meet. For example, private placement memorandums, Form D filings, and other offering documents

- Industry-specific regulations may also apply. For example, biotech/pharma companies may have additional disclosure rules around anti-dilution provisions.

- Some state laws restrict the use of full ratchet provisions or require specific disclosures. Companies should review regulations in states where they are incorporated or raise funding.

Disclosure Requirements

- Details of full ratchet provisions must be disclosed to all existing and potential shareholders. This includes explaining how the provision works and the potential impact on share value.

- Updates must be provided if the full ratchet terms are changed or triggered by a down round. Ongoing transparency is key.

- Proper documentation must be maintained and provided to shareholders if requested. Companies should retain legal counsel to ensure appropriate disclosures.

Tax and Accounting Implications

- Triggering a full ratchet provision may create a taxable event for shareholders if it materially impacts ownership percentages.

- There are specific revenue recognition and EPS accounting rules that apply to anti-dilution provisions which must be followed.

- Careful tracking of share ownership is necessary for compliance with tax rules related to equity compensation, options, and warrants.

- It is important to consult with advisors in tax and accounting when thinking of implementing full ratchet provisions.

Alternatives to Full Ratchet

Although this provision protects investors, it makes it more challenging for companies and founders. There are alternatives you can consider that might be able to balance out the interests of all the parties involved.

Pay-to-Play Provisions

With pay-to-play provisions, investors must join future funding rounds to avoid anti-dilution in their shares. This gives companies more certainty of funding while still providing investors some protection if they continue investing. This way, investors' shares would face dilution if they refuse to participate in future rounds. Therefore, they will keep investing to avoid an uncontrollable downward spiral. Companies may find this a fair compromise that makes fundraising easier.

Redemption Rights

Another alternative is granting investors redemption rights that allow them to sell their shares back to the company at a guaranteed price if certain conditions are triggered. This puts a floor value on the investor's stake while allowing the company flexibility on valuation. Investors can redeem their investment if the company underperforms while avoiding the dilution of a down round. Granting redemption rights is a way to provide downside protection without the potential extremes of full ratchet anti-dilution.

No Anti-Dilution Clause

Some companies may opt to have no anti-dilution clause at all in investment agreements. This avoids restrictions on founders and gives the company full control of future financing. However, it means investors take on greater dilution risk in down rounds. Companies with strong traction may be able to negotiate deals without anti-dilution protections. The lack of anti-dilution clauses gives companies more flexibility but less investor protection. For some startups, the trade-off is worth it.

The Future of Full Ratchet Provisions

Because of the emerging trends in the startup and VC landscape, full-ratchet provisions are used to protect themselves against anti-dilution in down-rounds. Other financing methods like crowdfunding and ICOs can complicate full-ratchet provisions due to the large investor base.

Some experts anticipate a decline in their use, as companies with more financing options may find the terms restrictive. Additionally, there is a movement toward more founder-friendly investment terms, potentially leading to pushback against full ratchets. Economic and market conditions will also impact their prevalence, with founders having more leverage during favorable periods. Balancing the interests of founders and investors remains an ongoing discussion, and the specific role of full ratchet provisions is still evolving.