In investment agreements, a "dilution provision" safeguards investors from losing their stake in a company when the firm offers shares at a reduced price in future funding cycles. This provision guarantees that investors maintain their ownership share and the worth of their shares thereby averting dilution. Should a company secure funds at a valuation lower than that of the previous rounds, existing shareholders may face a reduction in both their ownership interest and share value.

Anti-dilution provisions automatically modify conversion prices or ratios for shareholders, counterbalancing the effects of the reduced valuation. This method protects investors from a decline in their ownership portion. Anti-dilution clauses provide a safety net for investors when a company issues new shares at a lower valuation. They help investors retain their proportional ownership in the company.

Types of Anti-Dilution Provisions

The key difference between full ratchet and weighted-average lies in how each calculates the adjusted conversion into share price, for investors.

Full Ratchet Anti-Dilution

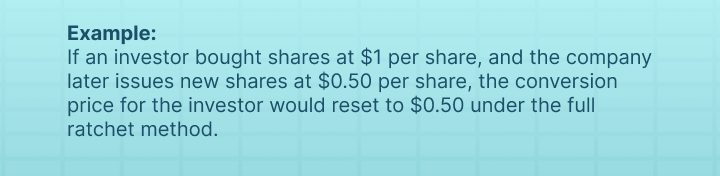

With a full ratchet provision, the conversion price of common shares outstanding in stock is reduced to the price of the new shares issued by the company. It is typically viewed as more investor-friendly.

This protects the investor from dilution but can significantly penalize the other company's ability by drastically reducing the original conversion price amount.

Weighted Average Anti-Dilution

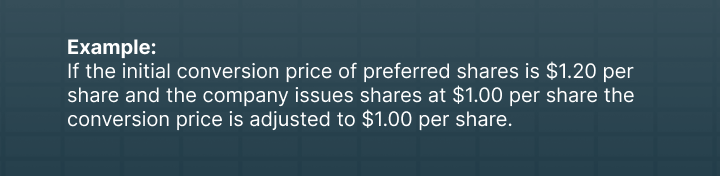

A weighted average provision considers both the old conversion price and the new share price when determining the adjusted conversion price of outstanding common stock. The investor's shares don't convert at the lowest price but rather a blended, narrow based weighted average based on relative share amounts. There are two sub-types under weighted average:

- Broad-Based Weighted Average - The total shares considered in the calculation encompass all assets such as options, warrants, etc. This approach is viewed as usually preferred by the company.

- Narrow-Based Weighted Average—Only outstanding shares and new shares issued are used in the calculation. This method is more protective of investors' interests.

The weighted average method provides a balanced outcome for both companies and investors. While the investor is still protected from unfair dilution, the penalty to prior investors in the company valuation is not as harsh as full ratchet.

How Anti-Dilution Formulas Work

Full Ratchet Formula

The full ratchet formula changes the preferred stock and shares conversion price to match the price at which new shares are issued in a round.

This safeguard benefits investors by enabling them to convert their outstanding preferred shares back into common shares. However, it can significantly move voting power and dilute the ownership of founders and employees.

Weighted Average Formula

The weighted average formula calculates a new conversion price based on the valuation cap of the current round and the previous round. The formula is:

- New Conversion Price = (A x B) + (C x D) A + C

- Where: A = Total number of shares prior to new round

- B = Price per share prior to new round

- C = Number of new shares being issues in the financing round

- D = Price per share of new shares in the financing round

- For example: Prior valuation cap: $1,000,000

- Prior shares outstanding: 1,000,000

- Prior conversion price: $1.00 per share

- New valuation cap: $1,500,000

- New shares issued in financing round: 500,000

- New share price: $0.80

- New Conversion Price = (1,000,000 x $1.00) + (500,000 x $0.80) 1,000,000 + 500,000 = $1,400,000 / 1,500,000 = $0.93

- So the conversion price is adjusted downwards to $0.93 per share.

The weighted average method is generally seen as more favorable to founders than a full ratchet.

Importance for Investors

An anti-dilution provision is an important tool for investors, especially those investing in a startup's equity financing at early stages. Here are some of the reasons why these provisions are so critical:

- Gives Confidence to Invest Early Stage: Investing in a startup during its stages carries more risk than investing in an established company. Valuations often hinge on speculation, and the company's future success remains unproven. This uncertainty often worries investors about the dilution of their stake. Having a dilution clause in position provides peace of mind to investors as their shareholding won't be significantly diluted. This builds their trust in investing during these volatile stages.

- Maintains Ownership Percentages: Investors might notice a reduction in their stake if a company secures funding at a valuation lacking an anti-dilution provision. These clauses reassure investors that their ownership stake will remain stable amidst dilution enabling them to predict returns with precision.

- Important Relationship Tool: When founders agree to include a dilution provision, it demonstrates their appreciation for the early investors and their commitment to safeguarding them against unjust dilution. This helps cultivate lasting connections between investors and founders, essential for future fundraising efforts. Experienced investors tend to approach companies cautiously if they're reluctant to offer dilution safeguards.

Overall, anti-dilution provisions provide investors with key protections and confidence needed to invest in high-risk startups. For founders, agreeing to such clauses shows commitment to treating early investors fairly.

What Startup Founders Should Consider

As a startup founder raising venture capital, you will likely encounter requests for anti-dilution provisions. Here are some key considerations when faced with negotiating anti-dilution clauses:

Pros of Accepting Anti-Dilution Provisions

- Helps build confidence in early investors to invest in high-risk funding rounds

- Shows investors you are committed to protecting their stake

- Anti-dilution clauses are considered standard, so they may be expected by sophisticated investors

Cons of Anti-Dilution Provisions

- Limits a company's flexibility and ability to raise future capital

- It can deter later investors who don't want earlier investors to get preferential treatment

- May signal a lack of confidence in future potential value to new investors

Tips for Negotiating Anti-Dilution

- Try to limit anti-dilution provisions to only 1-2 years after investment

- Narrow-based or broad-based weighted average is preferable to full ratchet

- Include carve-outs for employee shares or smaller raises

- Make sure repurchase rights are tied to specific reasonable triggers

- Seek experienced legal counsel to ensure a balanced, founder-friendly deal

In summary, while anti-dilution provisions favor early investors, as a founder, you still have the power to negotiate. You can secure clauses that protect investors while maintaining flexibility with the right counsel and strategic concessions. Finding the middle ground that makes all parties feel fairly treated is key.

Anti-Dilution in Down Rounds

Investors closely consider anti-dilution protections, especially in down rounds when a company receives funding at a lower valuation than the previous round. During these instances, anti-dilution provisions are activated to counteract potential dilution, by adjusting the conversion price for investors.

Let's say you're an investor who bought preferred shares in a promising startup at a $10 million valuation and $1 per share. Unfortunately, the startup faced challenges and had to raise funds in a down round at a $5 million valuation.

Due to the down round, your ownership percentage would be diluted because new shares are issued at the down round at a lower price. However, your agreement's anti-dilution clause, specifically a full ratchet provision, would protect your investment. This provision adjusts your conversion price based on the new valuation of the down round.

With a broad-based weighted average provision, the conversion price becomes the weighted average of the new number of shares being issued and total outstanding shares. This provides partial protection against dilution. Down rounds almost always trigger anti-dilution provisions if they are in place.

Investors specifically negotiate these clauses to avoid excessive dilution of their stake when companies stagnate or decline in value. Entrepreneurs should be prepared to expect these clauses in down rounds.

Key Differences Between Anti-Dilution in the US vs EU

Differences in the anti dilution protection in clauses exist between the United States and the European Union. In the US, these clauses are frequently seen in venture capital and growth equity funding, where institutional investors often seek protection against dilution. The full ratchet approach is prevalent among US investors.

In contrast, anti-dilution provisions are less common in the EU startup ecosystem. European investors are often willing to invest without such protections. The broad-based weighted average approach is more common when used in the EU. US startups raising a Series A round usually grant full ratchet anti-dilution protection, while comparable EU startups may not include any.

Furthermore, US courts are generally more inclined to enforce broad anti-dilution provisions than EU courts. Some EU courts have deemed certain anti-dilution provisions unfair and unenforceable.

In general, the significance of dilution protection is more pronounced in the US than in the EU. Investors in Europe tend to exhibit adaptability by incorporating dilution protection measures solely within particular high-risk contexts. Startups must recognize these variations across the Atlantic, especially when engaging in fundraising activities and navigating term sheet discussions.

Alternatives to Anti-Dilution

While anti-dilution provisions offer important protections for investors, other mechanisms can also help retain ownership percentages.

Preemptive Rights

An alternative to anti-dilution is preemptive rights, where current common stock or preferred stock shareholders can buy a share of any new company stocks issued to retain their ownership stake.

Preemptive rights allow shareholders to preserve ownership percentages without complex anti-dilution formulas and adjustments. However, shareholders generally must purchase these new shares, whereas anti-dilution clauses adjust preferred share conversion prices automatically.

Overall, preemptive rights provide an alternative mechanism to minimize dilution but do not offer the same downside protection as anti-dilution clauses. The choice depends on negotiations between founders and investors.

Key Takeaways

Investors use dilution provisions to safeguard their ownership stake from unfair dilution when companies issue new shares. Here are a couple of points to note when :

- These provisions automatically modify the conversion ratio in the event of a decrease in valuation, thus safeguarding existing shareholders from dilution.

- The primary categories include full ratchet, which adapts to the price, and weighted average, which adjusts based on a calculated average.

- A weighted average is generally considered more fair to founders and employees with equity. Full ratchet is viewed as punitive.

- Anti-dilution provisions incentivize investors to participate in follow-on rounds and give them confidence to invest early on.

- Startup founders should understand how these provisions work when negotiating term sheets. It's important to limit the scope.

- Broad-based weighted average anti-dilution is preferable for founders as it excludes convertible securities in the calculation.

- Anti-dilution provisions apply differently in the EU compared to the US due to stylistic differences.

- Keeping records of capitalization tables is crucial for monitoring shifts in share ownership and dilution across financing cycles.

- Although measures against dilution safeguard investors, founders must thoroughly evaluate the advantages and disadvantages before consenting to these terms.